The easy part is looking at why it’s happening; the hard part is getting through it.

This was not the Substack I originally wrote for the week but here we are…

By now you’re all reading news and headlines trying to understand what is happening with the market and your investments. The desire to understand is driven by the hope that if we can learn why something is happening, we can make it stop, or at least see when it will end. As every down cycle in the market reminds us, when it comes to investing—this hope is never fully realized.

Why is this happening to the market?

Here is a quick rundown on why the economy, and as a result, the market, is in a downward trend (trend is a nicer word than what we may feel which is—spiral).

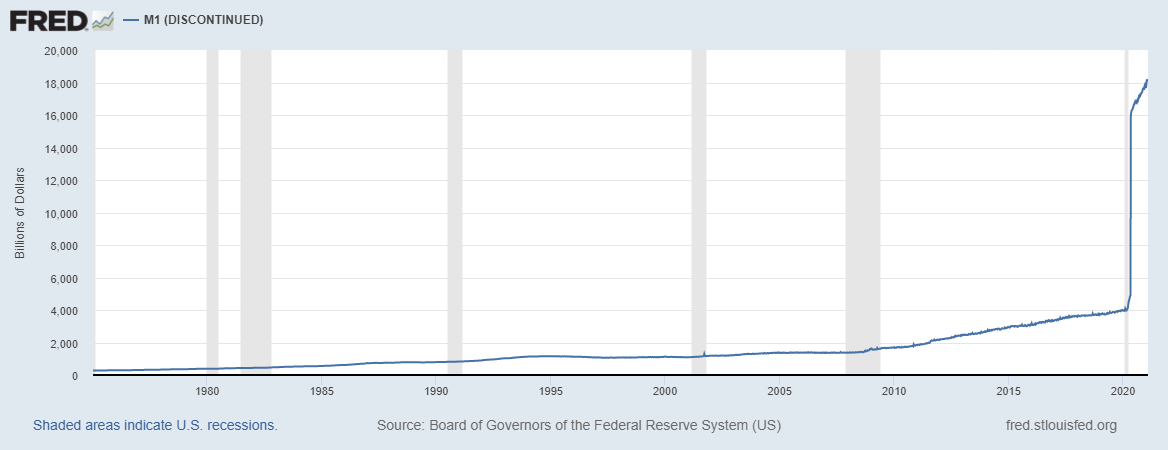

Too much money in the system will cause inflation. Before 2008 the amount of printing done by the Federal Reserve remained fairly stable. However, starting with the 2008 Great Recession the government increased the amount of dollars in the system in hopes of easing the nation’s downturn. Then, in 2020, spurred by the COVID pandemic response, the U.S. injected an unprecedented amount of money into the system.

How much money is printed in the United States. Notice an uptick in 2008 due to government involvement in that recession. The exponential increase in 2020 is due to COVID pandemic spending. Just like with anything, the more you have of something, the less it will be worth. This is how inflation has ticked up so rapidly. The inflation you are seeing is the outcome that follows an incredible about amount of money being added to the economy; our purchasing power (what a dollar can buy) is contingent upon how many dollars the Fed has in circulation. As anything, the more you have of it, the less it is worth.

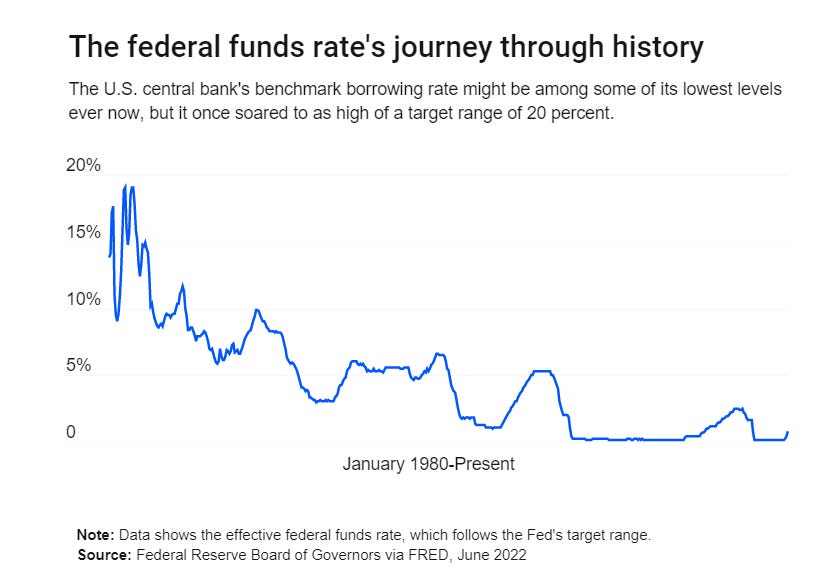

The Fed is raising rates to slow the money flow, hoping to reduce the inflation rate. When money is easily borrowed it is easily spent. If interest rates to borrow are enticing, investors will borrow monies they do not have, and put it towards assets they otherwise could not acquire. Over the last few decades, this has allowed investors to borrow money to buy assets and participate in the economy. Effectively, when you witnessed the record-breaking home prices and increases in the stock market, some of this was attributed to the easy access of borrowing.

By increasing the cost of borrowing monies, the Fed is hoping to slow down/reduce the amount of borrowing that is happening, which will in turn slow down investors inputting more money into the economy by borrowing. Ultimately, this slow down should reduce the inflation rate because less money is flowing. Think of money as a liquid. Over the last couple years, money was water—flowing all over the place. The Fed is hoping to make it molasses.

Investor sentiment plays a role, but not as substantial as the fundamentals above. Investor nerves plays a role, particularly in the daily stock market movements. People react emotionally with the trending downturn and sell assets they have invested—compounding the already downward trending market. (Sentiment also plays a role in market runups—people get excited to participate and start putting monies into an upward market, increasing its trajectory).

Other compounding factors. There are other factors potentially worsening our situation. Things like supply chain disruptions, shortages, and other influencing events. Many of these things will exacerbate the situation, but had they occurred in an otherwise healthy economy would have been simply an inconvenience.

What to do next?

While it’s comforting to think much can be done, it is an illusion. Even the Federal Reserve was unable to foresee this asset bubble and is now playing catch up desperately trying to solve the inflation problem. Down market cycles are part of the natural way the economic system corrects itself. While not what investors want to hear, they are key to moving to the next cycle of growth. Any system—not just market cycles—requires a way to rebalance itself routinely when things are not aligned to make it perform efficiently. In our current situation, the system cannot hand the overwhelming amount of monies and ease of spending perpetually, and thus it corrects itself while we wait.

Now here are the reminders; if you are a client, you have heard them, but they are worth repeating:

STAY THE COURSE. Market cycles are part of our long-term investment return projections. The only way is through.

Accumulators: If you are still working and investing—DO NOT STOP. Keep contributing to your employer plan and other investments. In fact, if you can increase your contributions, now is the time—you are buying in at lower price points.

Retirees: If you can delay any big purchases and reduce your lifestyle, plan on doing so. Selling positions now is not ideal, so minimize how much is needed to sustain your lifestyle until this cycle ends.